How Lenders Judge Creditworthiness

A car with all the updated features or a home to accommodate the family’s requirements, getting a loan for these reasons is a big financial decision. Fulfilling many more practical day-to-day needs with sufficient funds are the lenders.

They can be an individual, a group, or a financial institution that provides money to a person or a business to repay within an expected period. Even in a fluctuating market, they can help to complete many goals.

How do lenders analyze the creditworthiness of a person or estimate if he or she is eligible to pay the initial and complete amount with interest on time? A risk assessment by banks and understanding what is DTI are significant methods of estimation.

In this article, we will inform you of the necessary evaluation lenders conduct before providing funds to an individual or a business.

Diverse Lending Requirements

There are various lending factors and different loans with specific repayment options. From home, auto, banks, brokers, credit unions, retail, and many more types of lenders.

A company’s or a person’s eligibility is based on a financial portfolio consisting of past dues and current income stature.

Creditors utilize the DTI or debt-to-income ratio to measure debt payments against the pretax income. It is the percentage of income spent to pay dues every month. This is how it is calculated, and few rules to understand it.

- Divide total debt payment by your total income. The percentage will be the DTI ratio.

- The current income should be ongoing and fixed based on before-tax income and not the take-home total salary.

- There is no requirement to include every bill of your household, such as food and fuel.

- Include housing costs, any mortgage payments, and HOA dues.

- Any dues on credit cards and ongoing loans, like Student loan in Singapore, should also be part of the debt-to-income calculation.

A necessary thing to note is that the lower the DTI ratio, the better your chances of procuring a loan. A high debt level can be lowered by paying off debts or increasing your income.

THINGS TO CONSIDER

Many financial experts suggest lowering the number of credit applications within a short period, which can be seen as a high-risk borrower and impact your creditworthiness.

Annual and Monthly Credit History

Repayments impact the risk assessment directly, which can either build trust or lose value in the eyes of the creditor. Quarterly monitoring of your bank details always keeps a check on the accounts.

Having a fixed income source and timely payment of dues creates a good story of creditworthiness. Before lending funds, lenders do a detailed background check to verify every transaction and the way you handled them, including child support.

DTI helps banks determine the quantity of loans against any past dues that could impact the present or future repayments. A maximum of 36% DTI is generally understood to be a safe borrow, but more than that needs a re-evaluation of other assets.

Another determining factor is the credit history and overall credit score. The most common scoring model is the FICO credit score, which requires a range of 300 to 850. Paying all your debts on time is the best way to improve loan capabilities.

Evaluation of Current and Future Goals

It isn’t easy to evaluate personal and professional goals in a volatile economy that is still recovering from the Covid pandemic lockdown. It impacted many businesses and startups that had borrowed heavily and still were in the process of saving for health insurance.

However, the lenders also need a collateral asset along with the loan amount. This is specifically done for procuring home loans. The value of an asset determines the repayment ability of a borrower and to avoid any defaults, banks have to use collaterals.

Paying a heavy amount of down payment upfront or in the initial stages is also a great way to reduce interest rates on a loan. About 20% of the purchase price is a good percentage to create trust between the borrower and the creditor for future funds as well.

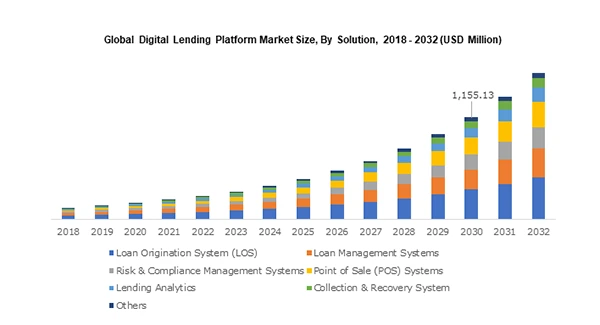

The graph below shows a new wave of creditors, which is called the digital lending platforms. Their start was slow, but consistently these global lenders have won the confidence of people.

Conclusion

If you are preparing to fund a huge project for a startup or planning to buy a new house, there are multiple ways to handle money. With savings and investment, the loan is a perfect way to complete all your goals.

Personal and student loans are the most common, but lenders help in every field. They assess past dues, credit history, repayments, credit score, and current income capabilities. An evaluation and constant monitoring by calculating DTI present a clear picture to confidently obtain loans for fulfilling your family’s dreams.

Also Read: How to Get a Bad Credit Car Loan