Fintech Innovations in Student Financial Management: Enhancing Borrowing, Repayment, and Financial Literacy

The fintech revolution has permeated the student lending sector as tech-focused startups build innovative solutions to streamline financial processes for student borrowers. New tools powered by artificial intelligence and big data analytics are transforming how students access funding, manage debt, and plan their financial futures.

You can start understanding the topic by taking your example in real life. To streamline your money-related knowledge and the whole process, several start-ups or companies are making innovations in the sector. These fintech innovations address common pain points across the student journey like yours – from securing loans and repayment to building financial literacy.

With that being said, this write-up is going to take you on a tour of such innovations.

Simplifying Student Loan Applications

Starting with the elephant in the room, applying for financial aid can be an enormously complicated process — navigating the FAFSA, comparing aid packages, securing private loans to fill gaps, and maintaining eligibility through school, involves complexity high enough to deter potential candidates. You may wonder, “How does student loan work when there are so many options and requirements?” Fintech apps aim to reduce that friction and improve accessible funding.

Thanks to platforms like Mos, Prodigy Finance, and Credible online marketplaces aggregate loan products for easy comparison shopping. Students like you describe their needs and receive personalized rates and terms from lending partners. Features like filters allow you to customize loan types, eligibility factors, and desirable features such as income-based repayment or cosigner release. Automated pre-qualification guides decision-making towards suitable products.

Income share agreement (ISA) providers such as Blair, LexieCap, and Meratas also facilitate alternative funding based on students’ future earnings potential rather than credit scores. ISAs require no payments until securing a job above an income threshold, with installment percentages scaling to actual salaries. Such innovative options expand access by aligning costs to personal circumstances.

Simplified loan applications help you secure necessary financing for school quickly and knowledgeably. Customized product matching eliminates hassles and confusion surrounding lending intricacies.

Streamlining Repayment and Reducing Delinquencies

Student borrowers often struggle to turn theoretical future payments into reality post-graduation. Due to this, income uncertainty, lagging financial literacy, and inability to prioritize debts lead to missed installments and delinquencies. Therefore, fintech apps promote responsible repayment by automating processes and providing flexibility.

Tuition.io, FutureFuel, and Gradvisor debit payments directly from your paychecks or bank accounts, splitting larger monthly dues into small, regular installments. It mimics payroll tax deductions when preventing missed payments and accruing interest. Similar platforms can also optimize across multiple loans, directing extra funds toward the highest interest balances first. Alert systems notify users of upcoming debits and payment totals to avoid overdrafts.

Well, in order to make the process more convenient for both you and the firm, if you lose jobs or face temporary hardship, platforms facilitate pausing or lowering your payments without damaging credit or risking default. And the moment when you get back stable, fintechs then restart regular payments after getting your finances back on track. This automating slack periods aid those struggling to consistently make traditional fixed payments.

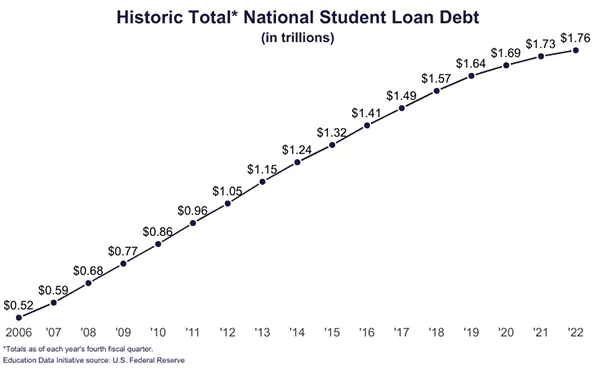

INTERESTING FACT

Here you can see the historical total amount of national student loan debt in the USA (in trillions).

Similarly, intelligent tracking, forecasting, and notifications further empower you to manage repayments smoothly. Platforms integrate with loan providers to centralize information across funding sources and project future balances based on various inputs.

Driving Financial Literacy and Planning

Many students lack the basic financial knowledge to guide borrowing and repayment decisions responsibly. Fintechs promote literacy and planning around long-term debt impacts through engaging tools.

Savvy platforms project loan costs over 10-25 years under different repayment schemes, calculating total interest accrued based on variables like career income trajectories. Visualizing future outcomes helps students make informed borrowing choices and model viable careers to manage debt through projected starting salaries.

Other apps build granular financial identity profiles analyzing spending habits, cash flows, and financial behaviors to detect risks or opportunities. Personalized insights allow early course correction towards healthy habits when in school, with tips related to balancing food delivery spending or strategically timing credit card payments to build credit. Gamifying lessons through points, badges, and rewards further drives sticky engagement, especially among Gen Z users.

Equipping students to take ownership over current and future finances promotes responsibility to prevent adverse lending scenarios down the road. Fintech innovations improve decision-making through practical learning.

Importance of Data Privacy and Security

Since the rise in fintech apps collecting and analyzing sensitive personal financial data, the privacy rights of students have become a major concern. In order to maintain trust, providers must be transparent regarding data usage during securing systems against breaches exposing that information. This can be done by adopting encryption, access controls, and ethical AI practices to build necessary trust in the fintech ecosystem. You deserve assurance your most private financial details remain protected, don’t you?

The responsible regulatory bodies should also look to balance innovation against consumer protection. This is where guidelines like GDPR come under the limelight. GDPR spells out fintech duties for securing and minimally processing their customer data. As business models rely on aggregating information across institutions into central platforms, upholding rigorous cybersecurity and privacy standards is necessary.

Fostering Inclusive Access

An unfortunate reality of higher education is persistent gaps in representation and achievement across student demographics. Thanks to rising tuition costs and loan burdens, minorities, first-generation applicants, and low-income groups remain underserved. In this situation, fintech innovations can specifically target more equitable access.

Simplified applications strive to reduce barriers deterring promising you from disadvantaged backgrounds. Alternative ISA funding models also help you if you lack traditional financial qualifications. Streamlining repayment eases stresses disproportionately affecting such groups. Literacy programs tailored to minority cultures or household constraints provide relevant money lessons.

Purposeful fintechs will measure success not just in efficiency but also in reaching students earlier left behind. Their futures stand to gain the most from innovation-expanding opportunities.