The Three Keys to Getting That SBA Loan

Small business loans are one way with which new entrepreneurs can gain financial support.

Finding a small business debt isn’t for the faint of heart. When you are frustrated by loan declines, look into SBA financing instead.

Although the Small Business Administration has stringent requirements for 2, it is also responsible for ensuring that small businesses nationwide have access to SBA loans.

In other words, you can usually bet on acceptance if you meet those requirements since SBA works with banks and other lenders. However, it guarantees up to 85 percent of loans they issue.

Finding the correct lender could take a few tries or involve lengthy wait periods, but in the end, it usually works out.

If you can demonstrate your compliance quickly and clearly, approval is more probable on the first attempt. Here are some ways to succeed.

Clearly and conservatively project your financial outcomes.

Some may be eager to take advantage of the chance to expand their firm after they have the necessary capital for large assets.

Before doing so, the SBA and the lender will want to know what the best and worst-case situations are.

All things considered, the marketing and operational sections of the company strategy ought to back up financial predictions.

They shouldn’t be too hopeful or too cautious, but if they’re confident in their ability to repay the debt—with or without the increased income it would generate from purchasing equipment or property—there’s no need to hold back.

Statistics:

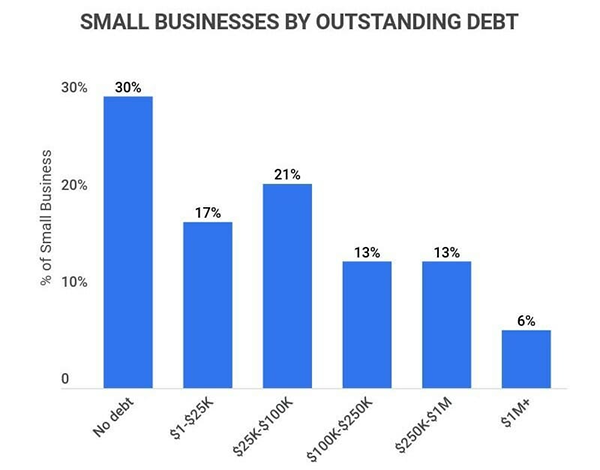

According to small business lending statistics, it is seen that most of the businesses with outstanding debt have balances under $100,000.

Whereas, 17% of small firms have debts of up to $25,000, and 21% have debts of between $25,000 and $100,000.

The objective is to demonstrate a high probability of repaying the SBA loans, regardless of how quickly the new assets generate profits.

Make sure the forecasts are fair and not negative in tone because of that aim.

Display Your Available Funds Without a doubt

To invest equity in the collateralized assets, the Small Business Administration mandates a 20% down payment from borrowers.

By including the company owner in the shared risk, the likelihood of the debt becoming underwater in the event of a default is reduced.

Do You Know?:

As per the data found, 82% of small businesses fail due to cash flow problems, 42% due to lack of market, 29% run out of cash, 23% due to having a mismatched team, and 19% are because of competition winning.

The funds for such payment must be available and distinct from the emergency funds required if income falls short.

The next step is to show how long one can purchase with their reserve cash before requiring a surge in revenues to keep the business afloat.

Maintain a Level Head When Asking for a Loan

If the lender determines that one will have trouble making monthly payments, that is the most common reason a debt may be denied.

You may avoid that by getting numbers straight and making sure the request is within the budget.

That way, everyone’s risk is low, and the down payment is little. When added to the other two pieces of advice, it will greatly improve the likelihood that the application will be approved.

Filling Out an SBA Loan Application

This is the proper format for a Small Business Administration loan application.

Gather all the necessary paperwork.

The following documents are necessary (among others unique to the bank):

- 3 years of business tax returns

- 3 years of personal tax returns

- A debt application that allows all owners’ credit reports

- Business debt schedule (BDS)

- Personal financial statement (PFS)

- Interim financials

- AP and AR aging reports

- Entity records

- Purchase contracts

It will be much easier if you can have everything in its proper place before you start.

Be warned: The lender will not make the necessary effort to complete the SBA construction loan if you skimp on this procedure. They won’t bother if you aren’t going to.

Speak with a commercial banker

The vocabulary employed by business bankers seems to vary per bank. At my banks, they’re called debt officers, business bankers, and business development officers.

Interesting Fact:

The average SBA loan size is $108,000 and the average interest rate for SBA loans is 7.75%.

Some banks use “catch-all bankers” to handle credit card and multimillion-dollar real estate transactions.

Larger financial institutions may have divisions dedicated to government-guaranteed lending.

Interview the lender to ensure they understand SBA loans. We recommend advising them to be honest beforehand. To avoid losing contracts, bankers routinely overstate timelines and requirements. Instead of expecting four weeks and getting six.

Complete the underwriting process

Two or three weeks may pass before underwriting is closed. Something is likely amiss if it isn’t sufficient.

Underwriting typically should take at most three weeks, however, it can take longer if the bank is experiencing heavy workloads, such as during a rate discount.

However, if your banker gets you into underwriting after only one week, you should be wary.

Although it is within the capabilities of certain lenders, the process of ordering appraisals, coordinating with the management team, and preparing the debt transmittal is lengthy.

Final Take

Conclusively, SBA loans can be more challenging to get done. Despite all the challenges, it can be vital for all the entrepreneurs seeking financial support.

Believe this, it could be the last resort.

Success in obtaining a Small Business Administration loan hinges on the keys mentioned in this article. Getting started with an application process requires attention to detail.

In essence, securing an SBA loan can greatly enhance the financial support needed for small businesses.