Loans and borrowings are noteworthy parts of any business operations. If the business operates on a large scale, it is not always possible to arrange money for launching big projects. Hence, loans become a much more viable option to carry on with.

If you own a business, a financier could give you an injection of funds. The average business owner has nowhere near enough money, so they are a great option. However, the process of applying for credit can be somewhat complicated. If you have never made an application before, the chances are you aren’t going to know what to do.

This post will simplify things for you, which it will do by explaining every step in the application process, as well as offering some tips for getting a good deal.

Different Types of Loan

The first thing you need to do if you are interested in applying for a loan to fund a new business venture or invest in a commercial project is to find a type that’s right for you. There are many types of borrowings, so understanding what they are can make it easier for you to find one that’s right. It’s possible to find title loans that don’t require the car, as well as those, that don’t require any kind of collateral. Here are the main types of borrowings that you need to know about:

Personal Loan

A personal loan is the most common type. Almost everybody has applied for a personal loan at least once in their lives. You can do just about anything with it, including using the money for your business. Something worth noting is that this type of credit typically has very unfavorable interest rates, so it’s not ideal as a long-term solution.

Business Loan

In case you are an aspiring entrepreneur but lack funds to start, a business loan can be a great option to consider. Usually, it is only given to people who are actively trying to start their own company, as opposed to established companies who are in need of a cash injection. Still, under the right circumstances, established businesses can still apply.

Secured Loan

A secured loan requires some type of collateral. Collateral is a physical item put up to secure the loan, i.e., a car or a house. If the defaults, the physical item is seized. This type of borrowing is commonly given to people whose credit scores are not good enough to warrant them applying for unsecured credit. They usually have better interest rates than personal loans, though.

Finding a Lender

If you are interested in applying for a loan, you need to find a lender that’s right for you. There are many lenders operating on the internet today, so find the one that is right for you. In order to determine if a lender is suitable or not, take a look at what people are saying about them on the internet.

Moreover, take some time to find out if they have gotten into trouble for unethical lending in the past. A simple internet search should tell you everything you need to know and bring up any relevant articles or posts.

Checking Credit Score

If you want to apply for a loan, start by checking your credit score. Your credit score is the main thing that lenders will use to decide if you are eligible for one of their products. Your credit report details all of your interactions with lenders and gives them an idea of how you manage your money.

You can check your credit score for free online. If it is not good, you may need to take out a secured loan. It requires collateral, as mentioned above. You do not have to have a good credit score to get a title loan or a credit that requires collateral.

Using Comparison Sites

When you are searching for credit, it’s paramount to use comparison sites. Comparison sites will compare different deals and help you find the best one for you. The use of comparison sites is highly prevalent among borrowers because they can be very insightful.

They will tell you which lenders have the best interest rates and also weigh up the pros and cons of working with certain lenders. Bear in mind some comparison sites are sponsored, which means they are somewhat biased. Still, they can be very informative.

Checking Interest Rates

In addition to using comparison sites, check interest rates before you apply for loans. Interest is added on top of the amount you borrow, so the higher the interest rate, the more you will have to pay back.

Bear in mind that interest rates vary from lender to lender, so shopping around can get you a good deal. Something else to note about interest rates is that the more you put down as a deposit, the lower the total amount of interest you will have to repay.

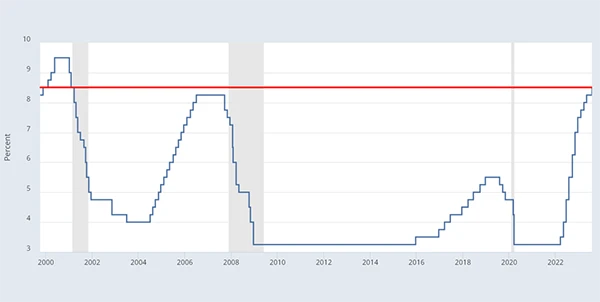

This graph showcases the interest rates in the USA across different times.

Guaranteeing Affordability

Before you borrow money, make sure you are in a good enough position to make each and every repayment. Missing even one can be very bad for your credit score. For example, defaulting can make it almost impossible to get credit for a period of up to six years.

Guaranteeing affordability is therefore necessary prior to applying for any form of credit. Making sure you are in a good enough position to make repayments can prevent any adverse credit incidents. If you can’t afford to make repayments, don’t take a loan out.

Making An Application

Once you have taken all prior steps referenced here, go ahead and make your application. The process is straightforward. Usually, loans are paid out the same day they are accepted.

However, if you have applied for a large business loan, you might have to wait a moment before your application is looked at. The same is also true if you are applying for a title loan and have bad credit. Any concerns or queries you have should be addressed directly to the lender that you want to work with.

Borrowing money can be an effective way to fund new business ventures or projects. However, it’s necessary to shop around and find the best lender you can, so you get a good deal. Don’t rush the process, because it can have a negative impact on your life and credit score if you do.