Targeting the Unbanked Market in Asia With Direct Carrier Billing

Jump To Key Section

- The Challenge of Reaching the Unbanked in Asia

- How Direct Carrier Billing Works in Singapore’s Mobile Market

- Top Benefits of Direct Carrier Billing for Asian Businesses

- Common Challenges and How to Overcome Them With DCBPays Singapore

- Practical Strategies to Launch and Grow Direct Carrier Billing in Singapore

- Conclusion

Many people around the world don’t have access to general banking services.

An innovative way to serve their financial needs is Direct Carrier Billing (DCB). This method involves paying for digital services through your mobile balance. It’s simple, secure, and covers a considerably larger population than banking services.

Businesses offering this payment method in unbanked or underbanked regions can easily overcome the lack of financial infrastructure and literacy.

There are some technical and regulatory barriers to the implementation and deployment of the system, but the demand and benefits are so great that it is getting really common in those regions. Another factor for that is the mobile phone penetration being very high. Almost half of the DCB market (49%) rests with the Asia-Pacific region (Source).

One such provider is DCBPays Singapore, which has opened new markets and strengthened financial inclusion across Asia.

In this article, I’ll discuss the unbanked population in Asia and DCB in detail. The following section lists the benefits and challenges of implementing DCB for the unbanked in Asia. In addition, there is a robust strategy to launch a DCB there, maximizing those benefits and minimizing the barriers.

KEY TAKEAWAYS

- High mobile penetration makes Asia a perfect market for direct operator billing for the unbanked.

- It allows people to pay for digital services through their mobile phone balance or bills.

- Formulate a robust DCB deployment strategy, keeping in mind the implementation challenges.

The Challenge of Reaching the Unbanked in Asia

Asia has progressed at an unprecedented pace in the past few decades. Still, a considerable population lives and manages their finances without a proper banking system. They are called unbanked.

Limited physical banking infrastructure, strict documentation requirements, and low financial literacy continue to restrict many individuals from participating fully in the formal financial system.

In rural and remote regions, geographical challenges further complicate outreach efforts.

As a result, many rely on informal or cash-based transaction methods, limiting economic mobility and access to digital services. These barriers reduce participation in the digital economy and prevent millions from accessing secure payment solutions.

Addressing this gap requires alternative payment mechanisms that bypass conventional banking requirements while maintaining security and reliability.

How Direct Carrier Billing Works in Singapore’s Mobile Market

As mobile phone usage covers almost the entire population, the digital infrastructure already exists in Singapore. Deploying solutions like DCB through this medium makes it easy.

Direct Carrier Billing enables customers to charge their digital purchases directly to their mobile phone bills or balances.

The process typically works as follows:

- A user selects a digital product or service within an app or website.

- At checkout, the user selects DCBPays Singapore as the payment option.

- The amount payable is billed with the mobile or deducted from the balance.

- The mobile operator processes the payment and transfers funds to the merchant.

By removing the need for credit cards or bank accounts, this model simplifies digital transactions and aligns with Singapore’s highly mobile-driven consumer behavior.

Top Benefits of Direct Carrier Billing for Asian Businesses

The popularity of DCB is increasing manifoldly as many D2C businesses are adopting the payment method, widening their reach with the simple solution.

By removing reliance on traditional banking systems, DCBPays Singapore allows companies to engage previously excluded unbanked and underbanked populations. This increases customer accessibility and drives higher transaction completion rates.

Key benefits include:

- Broader customer reach without banking limitations

- Faster and real-time payment confirmations

- Reduced payment friction and cart abandonment

- Lower exposure to chargebacks compared to card payments

- Effective support for microtransactions and digital content monetization

Through DCBPays Singapore, businesses gain a scalable solution that enhances both revenue potential and customer inclusion.

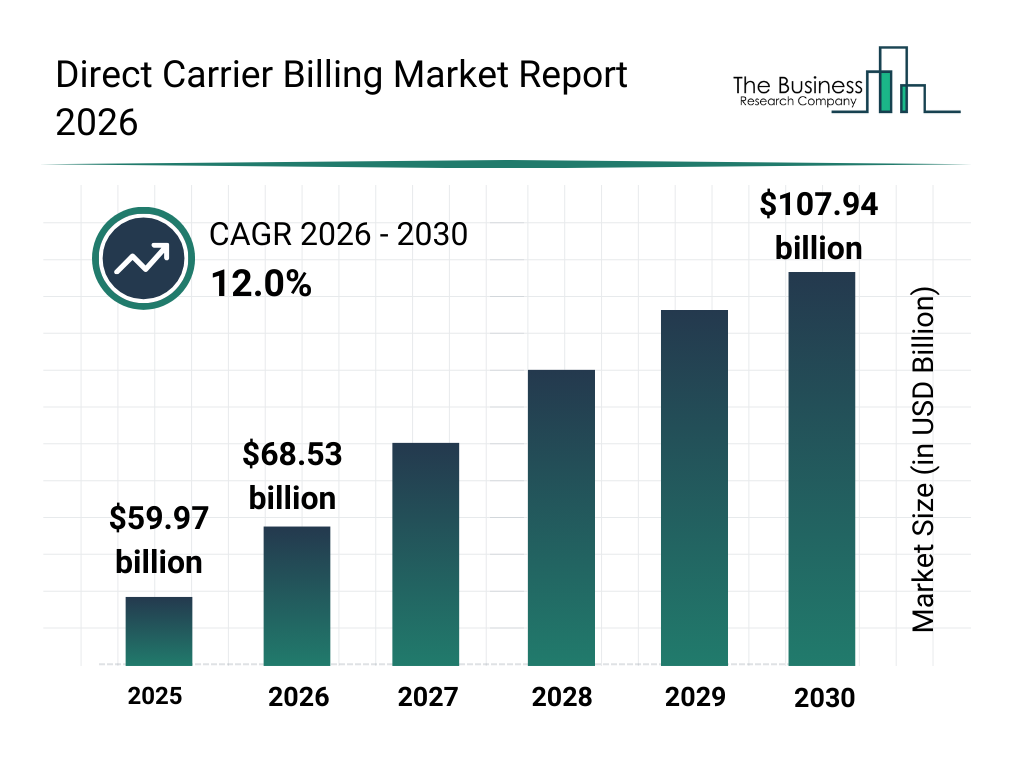

The following infographic shows the size of the DCB market along with the growth and potential it holds for the next 5 years.

Common Challenges and How to Overcome Them With DCBPays Singapore

The DCB system has many benefits, but there are some challenges as well in implementing and deploying it throughout Asia.

For example, regulatory compliance. You have to thoroughly research and understand the financial and telecom legal requirements for every country during the planning phase of the DCB system launch. Technical integration across multiple operators also demands flexible and secure backend infrastructure.

Fraud prevention is another key concern. Secure authentication protocols and carrier-level verification systems are necessary to maintain user confidence without creating excessive friction.

Educating consumers about the benefits and security of DCBPays Singapore further supports adoption. Strategic collaboration with operators, compliance experts, and payment technology partners ensures smooth implementation and sustainable growth.

Practical Strategies to Launch and Grow Direct Carrier Billing in Singapore

Deploying DCBPays Singapore is considerably easier. The vast digital infrastructure already exists in Singapore. You just have to partner with the telecom operators.

Close collaboration with operators ensures seamless integration and access to a wide user base. The billing should be transparent and promptly notified to build trust and confidence in DCB among users.

Transparent pricing and clear billing notifications help build user trust and improve payment confidence.

Localizing user experiences—such as offering multilingual support and simplified onboarding—encourages broader adoption. Continuous monitoring of compliance requirements ensures operational stability in Singapore’s structured regulatory environment.

Finally, targeted marketing campaigns that emphasize convenience, security, and accessibility can effectively attract mobile-first consumers.

Conclusion

DCB has transformed how Asians pay for digital services forever. The unbanked population has especially benefited from the innovative solution.

By simplifying payments through mobile carriers, businesses can overcome traditional banking barriers while expanding their customer base.

Although regulatory and integration challenges exist, structured implementation and strategic partnerships make operator billing a viable and scalable solution.

Ultimately, DCBPays Singapore enables businesses to unlock underserved markets, improve payment accessibility, and support broader financial inclusion across Asia’s growing digital economy.

Ans: Well over 1 billion people.

Ans: DCB is a secure, cashless payment method that allows people to pay for digital products and services through their mobile phone balance or bills.

Ans: Asia has a considerable unbanked population, while mobile phone penetration and usage are pretty high.