Do you know that 11.4% of total automobile loan applicants were rejected in 2024? (Fortunly: Car Loan Statistics) Yes, navigating through the world of car finance can be challenging, but it becomes even more difficult for those who are in an Individual Voluntary Arrangement (IVA).

It can be a struggle, but the good news is that there are still ways to get a vehicle loan even if someone is in the middle of an IVA or has recently completed one. If you are also in a similar situation, this post is for you.

Here, we will discuss everything you need to know about IVA, what it is, its impact on credit score, and what financial options are there to help someone get car finance in such situations. You can compare IVA car finance plans with CarMoney broker, among others, to make an informed decision.

Now, without further ado, let’s start with today’s topic!

KEY TAKEAWAYS

An Individual Voluntary Agreement (IVA) is a contract between an individual and a creditor.

Getting car finance during or after an IVA can be extremely challenging.

There are various options available to get a car loan with an IVA.

By following certain tips, you can increase your chances of getting an automobile loan after an IVA.

What is an IVA?

An IVA (Individual Voluntary Arrangement) is a contract between an individual and a creditor to repay parts of their debts over a fixed period of time (usually for five years). It is a formal debt solution for people with large sums of debt.

In most cases, once the terms of the IVA are completed, any unsecured debt left over is written off.

This arrangement can prove to be a lifesaver for those in financial distress; at the same time, it can have a big impact on the credit rating. It remains on the credit file for six years, and during that time, it becomes extremely difficult to get traditional forms of credit.

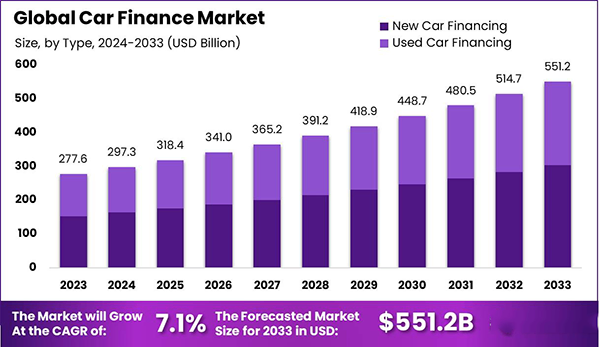

DO YOU KNOW? As of 2025, the global car finance market is worth USD 318.4 billion, it is projected to grow at a CAGR of 71% and reach $551.2% by 2033.

How an IVA Affects Your Credit

The most noticeable and immediate effect of an IVA can be seen on the person’s credit score. The credit gets marked as ‘affected by IVA’ for the whole arrangement period and even after it ends. Lenders get a bit reluctant to provide loans to those with such credit scores, including car finance applications. Making it harder to get approval for car finance if they are still in the middle of an IVA.

However, its effect on the credit can be temporary. After its completion, individuals can begin to rebuild their credit over time by showing financial responsibility, including paying bills on time, reducing outstanding balances, and avoiding debt in the future.

Car Finance Options During an IVA

Getting car finance while in an IVA can be challenging, but it’s not impossible. Some of the options available, each with its own pros and cons, are:

Guarantor Loans: Guarantor loans are secured by someone who agrees to pay the debt if the borrower can’t. A close friend or family member can act as a guarantor.

Secured Car Loans: In a secured loan, the car is used as collateral to borrow money. The drawback here is that it involves the risk of losing the vehicle if the debtor does not make timely repayments.

Bad Credit Lenders: Some specialist lenders even offer finance to individuals with a bad credit record, including someone in an IVA. They are aware of the borrower’s situation and are more likely to approve a loan, but at a higher interest rate.

These are some of the options, though they have their downsides, they can prove to be immense help when needed.

Car Finance Options After an IVA

The credit score may still be affected, even once the IVA is completed. Still, it’s comparatively easier to get car finance than when the IVA is active. Here are some ways to get back on the road:

PCP and HP Deals: Personal Contract Purchase (PCP) and Hire Purchase (HP) are two of the most common car finance options. Both allow the individuals to pay for the vehicle over time, with a mandatory upfront deposit.

Leasing: For those looking for an option with lower upfront costs, car leasing is the way. These agreements usually come with mileage restrictions, but they prove to be a good way to get a new car without needing a large deposit or long-term commitment.

Bad Credit Lenders: Many financial institutions specialize in providing loans to individuals with poor credit scores, helping those who are out of an IVA and are working on their credit. Though the terms may not be as favorable as with traditional financing, it can be an effective method to get a car loan.

Tips for Improving Your Chances of Approval

As we have established, getting a car loan during or after an IVA can be a bit difficult. There are several steps that can be taken to improve the chances of approval:

Save for a Larger Deposit: Bigger deposits reduce the amount required to borrow and enhance the chances of approval. This helps lenders understand if the client is financially responsible and committed to the purchase.

Check the Credit Report: Keeping the credit report up to date and ensuring that there are no errors that could have a negative impact on the application. In case of any discrepancies, get them corrected before applying for finance.

Be Transparent: Be upfront about the IVA and the measures that have been taken to rebuild the credit. Lenders are more likely to work with people who take proactive steps to improve their financial position.

INTERESTING TIDBIT Car financing started with the General Motors Acceptance Corporation, circa World War

Why Use a Car Finance Calculator?

A car finance calculator can help simplify the process of comparing car finance options during or after an IVA. It easily compares different finance plans to locate the best deal available, based on the client’s budget.

All that’s required to be put in is the car’s price, deposit amount, and loan term, then see what monthly repayments would look like for different finance options. This way, individuals would be able to make a more informed choice, especially if they’re considering a secured loan or a PCP deal after an IVA.

Final Thoughts

Yes, it’s true that an IVA certainly makes securing car finance a struggle, but one should know that it doesn’t have to be the end of the road. It doesn’t matter if someone is still in an IVA or has recently finished one; various options are available to help them finance a vehicle.

But, remember that it is important to understand the impact of an IVA on the credit score. Tools like a finance calculator can further help by comparing IVA car finance plans and finding a deal that best suits the borrower’s needs and budget the best.

Frequently Asked Questions

Ans: Yes, there are several options available to get a car loan during or after an IVA.

Ans: An IVA stays on your credit report for six years after its completion.

Ans: After the completion of an IVA, your debts are written off.

Ans: The fees for an IVA are quite high, so if your total debt is less than 10,000 euros, it might not be a good option for you.