Step-by-Step Guide to Disputing Errors on Your Experian Credit Report

Can you imagine the stress of having car repairs, home repairs, medical bills, and needing to pay college tuition all at one time? It’s a lot! It’s stressful! And truly in such a situation, most people don’t have thousands of extra dollars to put toward several unforeseen situations all at once. They end up having to borrow the funds or acquire credit cards to cover the difference.

Borrowing the money and paying it back later seems like a reasonable solution, however; the reality is that if you don’t have good credit, securing a loan or lines of credit may not be available to you. Moreover, if consumer reporting agencies (CRAs) like Experian make mistakes, it can cost you big time!

If you find yourself in this situation you will need to know how to dispute Experian credit report errors – FAST! We can help with that. We provide a step-by-step guide that will help you dispute Experian credit errors.

Below are the steps you should take to correct Experian credit report errors:

Step 1: Obtain Your Credit Report

You are entitled by law to receive your credit reports. You can get your credit reports online at annualcreditreport.com. Likewise, you have a right to receive credit reports from all three major consumer reporting agencies.

This means you have an opportunity to review each report for discrepancies that Experian must fix. It’s a good practice to review your reports every year (sometimes more often) depending on the circumstances. Reviewing your credit reports frequently helps to ensure that you are keeping up with any discrepancies or errors that may be found in your report.

Since time is of great importance when filing credit error disputes, reviewing your reports regularly can help you catch any errors quickly before too much time passes by.

Step 2: Identify Inaccuracies

Once you get your credit reports, review them carefully. Sometimes people will overlook what appears to be a “small” error like a misspelled name, but you should not overlook these errors. Any error, no matter the size, must be corrected.

Be sure to highlight and pinpoint these errors because you will need to mention them in your dispute letter. All errors (regardless of size) can play a part in your credit score decreasing and causing you to lose opportunities for financing, employment, and the life you deserve!

Step 3: Gather Relevant Documents and Other Evidence

Look for documents that support your dispute. These documents can be financial, legal, and loan documents, contracts, transcripts, leases, etc. For example, if Experian makes a mistake and reports you as deceased, you can provide documents showing that you are alive.

Or, if Experian reports a bankruptcy on your file, but you have never filed for bankruptcy, a letter from bankruptcy court stating that there is no record of you ever having filed bankruptcy will help prove that Experian erred.

Again, any related documents that help prove your case and dispute Experian’s mistakes will be relevant.

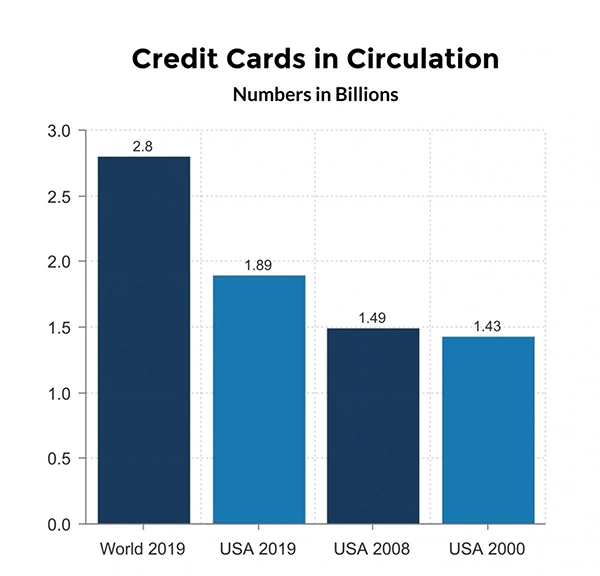

FUN FACT:

Here, you can see how massive the demand for credit cards is in the USA alone.

Step 4: Write Your Dispute Letter

The dispute letter is a very significant piece to your error-distributing puzzle. The dispute letter is what Experian and other CRAs will review. This letter will emphasize Experian’s mistakes and highlight why they are mistakes, and what you would like to have happen (like reinvestigation).

Moreover, you will have to provide information like your address, Social Security number, and other pertinent contact information so Experian can locate your file and investigate the dispute for you.

You can find example dispute letters online via the Federal Trade Commission’s website or you can contact consumer law attorneys and we can assist you with your dispute letter and the dispute process.

Step 5: Submit Your Dispute

Once your dispute letters are written, it is time to submit them (preferably via certified mail to preserve your legal rights.)

Certified mail is recommended because sometimes filing disputes online will require you to waive major rights that filing via certified mail does not require.

Therefore, we suggest certified mail as the preferred dispute method.

Plus, certified mail allows you to track when the letters have been delivered to Experian because it requires a signature.

Therefore, you will know who signed for the disputed letters, and on what day they signed for them, and you will be notified once the letters are delivered. Dispute letters for Experian should be mailed via certified mail to: Experian, P.O. Box 4500 Allen, TX 75013.

Step 6: Contact Legal Professionals

Contacting legal professionals who can assist you is often a good starting point, but it’s not too late to do this even if you’ve started the dispute process.

You can contact consumer protection attorneys at any point in your dispute process because we can meet you where you are.

It’s noteworthy that federal laws are in place that require Experian and other CRAs to investigate your dispute within a certain time frame. Typically, the investigation will take between 30 and 45 days. However, in some instances, the investigation will be complete in less than 30 days.

Additional Tips

If you don’t hear back from Experian within the required timeframe, you have a legal right to take further action.

Unfortunately, some consumers allow this to go unchecked and credit bureaus can escape responsibility for the credit report errors they’ve caused.

You should not let this slide. You are your best advocate and Consumer Attorneys are your ally in holding Experian accountable for their mistakes.

And, you have a right to rest easy knowing that your credit report is not filled with errors causing your score to drop and preventing you from securing financial assistance and living the life that you deserve!