Transforming Loan Underwriting: The Power of Technology

Alt: Loan underwriting technology

KEY TAKEAWAYS

- In the beginning, loan underwriting was done manually; after the emergence of AI-based tools, it became more accurate and secure.

- Human touch is still an irreplaceable element during the loan process, to make empathetic decisions.

- Both the tech and human elements that reduce biases could be done by agents.

- The underwriting process will be smarter and retain more borrowers in the future.

Did You Know? Federal Deposit Insurance Corporation’s 2024 report says that 42% of large banks have adopted financial technology (fintech) solutions for loan processing. Besides, another 31% of banks are also exploring new technical solutions for other banking processes.

The above shift clearly shows how significantly digital technology is entering the financial sector. Besides the large banks, small lender groups are also including this fintech to make the underwriting process easier.

Since the loan underwriting is transforming, every lender and borrower should be aware of these shifts and their outcomes. This will help them take advantage of this technical integration accurately.

Here comes this written guide, which explains its evolution, benefits, and its future. Don’t wait, just scroll down and read the whole article now.

The Evolution of Underwriting

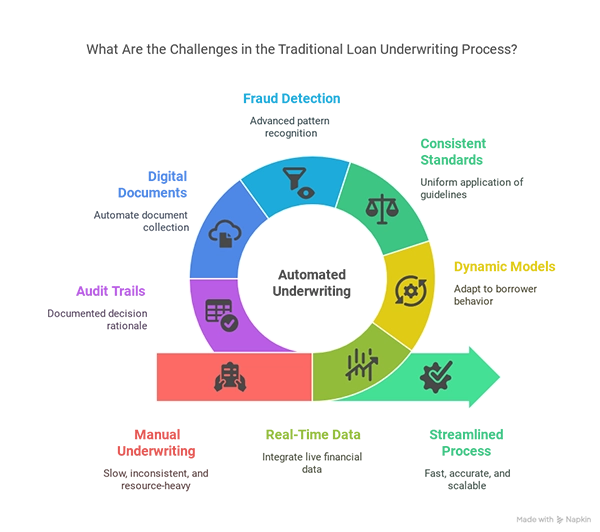

The underwriting process was completely different 15 years back in time. It was a slow and manually done work in the beginning, where underwriters used to pore over endless paperwork. Later on, the paperwork shifted to computer spreadsheets. However, both approaches were time-consuming and not very accurate.

Apart from the evolution, there were challenges in the traditional underwriting process, shown in the infographic below.

Finally, the time came when tools and AI innovation got involved in the operation, and the process began to transform effectively.

How Technology Powers the Transformation

The entire underwriting procedure started transforming after the arrival of smart technologies. This advanced system starts working when a loan application is received. It involves collecting different sources such as credit score, income, and much more.

Beyond that, artificial intelligence now saves hours of human labor and ensures a clear picture of an applicant’s profile. This is done with the help of powerful algorithms that spot patterns in data, making it easier to detect risk or determine the potential candidate.

This way, customers find more consistent lending decisions and a better experience. Also, lenders can feel more confident about their choices.

INTERESTING FACT

“The early roots of the term ‘underwriting ‘ originated with Lloyd’s of London in 1750.”

The Human Element in a Tech-Driven World

A human is still a very important and irreplaceable part of the loan underwriting process. Even after such AI technology, no algorithm can match human insights that add a sense of understanding. Only human agents can understand the unique situations, including family emergencies, career shifts, or other life events.

A personal loan underwriter professional can bring empathy and context to the work. For example, an applicant’s credit score went down because of a severe medical condition, so a human underwriter can investigate deeper and check current financial ability.

On the other hand, the completely automated system might have rejected this application just by seeing the credit score.

Benefits of a Tech-Enhanced Process

As the technology is becoming more advanced, the process is also improving. Moving ahead to break down the benefits for both lenders and borrowers, right below.

For Lenders:

- More applications get checked by automated tech.

- Digital systems reduce paperwork and manual errors, saving money in the long run.

- AI spots risky applicants or fraud quickly.

- Deeper digital insights provide better loan decisions and smart lending strategies.

For Borrowers:

- Less waiting because the application gets checked within hours.

- Automatic data-based decisions eliminate human biases.

- Digital upload makes the process simple and reduces overwhelming paperwork.

- Option to track application status online at any time.

Whether it is a lender or a borrower, tech has made underwriting simple, faster, and fairer. This way, both sides have a feeling of relaxation, receiving better outcomes.

Loan Underwriting Continues to Evolve

No one can disagree with the statement that loan underwriting will continue to evolve. As a fact, we have already seen tools that can read lines of application documents and blockchain systems, along with more secure transactions.

Based on the current events, looking ahead in the future gives a glimpse of a blend of new tools with trusted practices. It may include focusing on the borrower while being aware of regulatory changes and market trends.

Lenders are also realizing the value of personalization, so instead of using one criterion, they may use multiple techniques to modify loan decisions according to each person’s unique story.

In conclusion, underwriting has always kept evolving from manual processes to AI-driven technologies. But at depth, it will always be about human professionals understanding the borrower’s needs and dreams to turn them into reality. Overall, the future seems bright, and it would be smarter to just keep adapting to the changes.

Frequently Asked Questions

Ans: Loan underwriting is a process of checking the eligibility of a person to borrow using their income, credit history, and assets to make sure they can repay.

Ans: Absolutely not, just because technology has made underwriting faster doesn’t mean it can replace human understanding and personal touch in situations.

Ans: Due to advanced technology, some loan requests can be approved within hours, while other big loans can take up to weeks.

Ans: It uses credit score, income, past payments, and some other spending habits to decide the eligibility of clients.